As a "Cassandra", I would be remiss if I didn't offer some more general predictions for the coming year 2007 - particularly the kind that hopefully will stimulate debate because they are contentious. Of course, as the legend goes, few will believe them irespective that many will come to pass....

1. US Housing "Crisis" will be shallower than pessimists believe.

This one is easy. So long as central banks accumulate reserves, allowing US deficits to persist and grow coincidental to stable interest rates, economic growth will NOT implode and nominal house prices will stabilize preventing the apocalypse - at least for the moment. This doesn't mean "Buy Homebuilder Stocks", but it does mean that if one was considering purchasing a home, one shouldn't fear that he bottom will drop out further. Rather nominal tides will rise to float most boats.

2. "Intermediate Frame Price Momentum" will continue to be a factor that strongly contributes to Stock Returns in Japan.

Contrary to popular belief, wisdom, and experience, what outperformed in the recent intermediate frame will continue to outperform. This will, be due to a combination of continued money flows by investors alreadyh invested in japan alongside continued earnings growth of enterprises that have been experiencing earnings growth. This unspide-down world (for Japan) will perplex reversion-oriented traders, and reward trend-followers, however,, hollow and shallow theior relative intellect may be.

3. Contrary to contrarian calls by KBC's Jonathon(!!) Allum Dec07 Topix ~15000 call (note: this was incorrectly referred to originally as Nikkei~15000 -ed.), the Nikkei will rally to 20,000 and the TOPIX will rally to 2,000 (not necessarily in that order).

BOTH Large cap and small cap will rally as Japanese asset prices continue to look both relatively and absolutely attractive on a world stage where the only action is inaction."God Bless Apathy!" said one long and leveraged English Hedge Fund Manager

4. PM Abe will visit Yasukuni

....but he will do so under the cover of darkness. Unfortunately papparazzi will not be denied and yet another Japanese Prime Minister will once again have to explain the inexplicable.

5. California's official sponsorship of Universal Healthcare will prompt national debate on the compelling wisdom of universal healthcare, and the even-greater wisdom of a single-payor

Shares of HMOs will tank as the market begins to conceive of a healthcare world less-intermediated. America will receive [unwelcomed by Conservatives] advice from France on systemic reform, and as in 2003, America will again harass and fun of the Frenc, despite the wisdom and correctness of their advice.

6. US dawdles Yet Again on Energy Policy - Oil avgs $75bbl in 2007

The side effect of continued US deficits underpinning global demand combined with stubbornly pig-headed lack of energy policy and no carbon taxes is energy prices stay firm, and rally. At least once during the year, a crisis will cause a spike in crude to within a millimeter of triple digits. Refining margins will NOT deteriorate, and Valero (ticker VLO) will return 50%. Nippon Oil will be a stand-out investment in Japan also appreciating 50%.

7. Wolfowitz is Impeached and Relieved of Command as President of the World Bank

"Mutiny on H-Street" it will be called. The only thing more stupid than placing John Bolton in a diplomatic position was ejecting Paul Wolfowitz from the Pentagon to the helm of the World Bank. Many are still pinching themselves (those that haven't resigned) perplexedly asking themselves "How did HE get here??!?" OK its too early to say "things are right as rain", but little by little in bite-sized moresels, the good guys are reclaiming control, to the eventual benefit of humankind.

8. "The Carry Trade" Makes it to the Cover of Time Magazine

No major move on the RmB. Pathetically small increases in the BoJ discount rate. No move in US fiscal or monetary policy. No GCC currency appreciation. Continued reserve accumulation of USDs by all the usual suspects. All will mean the carry trade lives. It will make the cover of time magazine because a hedge fund manager consortia in partnership with a private-equity consortia will propose to take the entire remaining S&P 500 private, using - yes, you guessed it - YEN financed funds from Japan. This will get Congress to hold hearings, at which Rep. Barney Frank will chide Lloyd Blankfein & John Mack for "shitting on their own dinner plates by facilitating and participating in the "Stealing of America's Assets".

Wednesday, December 27, 2006

How to Hide an Elephant - (Update)

If only my market-timing were so good! Just last week in the previous post in fact, Cassandra detailed the (oh so brief) history of reporting transparency in the Japanese equity market, leading up to an observation positing that "the elephants" (FMR, Cap Research, etc.) and the large-but-simply-paranoid have been employing "new" techniques to non-report their market pecadilloes.

Well this morning new regulations will take effect, according to Bloomberg, whereby authorities will be demanding that holders of greater than 5% positions are now required to file position updates twice a month. This apparently is in direct response to the rather un-cricket rule-bending discovered by authorities in their investigation of Takefumi Horie and the Livedoor affair. While any loophole-closing is better none (at least in Cassandra's view), this doesn't address the specific loop-hole of transactions that, in spirit confer ownership, such as swaps, OTC option-like structures that are employed for, and priced as if there were no other reason for the transaction than to to accumulate a position without triggering disclosure.

A big test will be at this year-end to see who, with the large position, is increasing their holdings (and as a result the stock price of said holdings) into the mutual fund bonus measurement period and the hedge fund calendar year-end. Anyone care to guess who'll win the ignominimous award of being the most blatant?!?!

Well this morning new regulations will take effect, according to Bloomberg, whereby authorities will be demanding that holders of greater than 5% positions are now required to file position updates twice a month. This apparently is in direct response to the rather un-cricket rule-bending discovered by authorities in their investigation of Takefumi Horie and the Livedoor affair. While any loophole-closing is better none (at least in Cassandra's view), this doesn't address the specific loop-hole of transactions that, in spirit confer ownership, such as swaps, OTC option-like structures that are employed for, and priced as if there were no other reason for the transaction than to to accumulate a position without triggering disclosure.

A big test will be at this year-end to see who, with the large position, is increasing their holdings (and as a result the stock price of said holdings) into the mutual fund bonus measurement period and the hedge fund calendar year-end. Anyone care to guess who'll win the ignominimous award of being the most blatant?!?!

Friday, December 22, 2006

How Do You Hide an Elephant

Being a fly on the wall means that sometimes one has to make conjectures, hypotheses, and suppositions in order to attempt to make sense of the world. For things are often not what they seem.

And, nowhere is this more germane than in the case of reporting large positions to stock exchange regulators around the world generally, and in Japan particularly. Japan seemingly has a love-hatre relationship with transparency. Reading who has bought what and when was a fascinating exercise. On one hand, ownership changes were only detailed twice a year, and even then, only the larger holders either through the YuHo or Toyo Keizaei. So it was long after the fact that one realized who had bought the slugs of stock that vaulted the price an issue by triple digit percent. Yet, at the same time, turnover identification was available on each stock at the end of each day. This was a dead give-away as to whether purchasers were foreign or domestic, sporadic or persistent. The strange mix of obfuscation and transparaency juxtaposed each other.

A few years ago, the authorities decided, for unexplained reasons, not to "fix" this, but to turn it own its head, by eliminating the revelation of who was responsible for what percentage of turnover in a security on a particular day, while instituting a requirement to report ownership positions in a security greater than 5% (and thereafter) within some timely interval that is apparently indecipherable when reviewing the very wide variety in reported actions and compliance. Now, one couldn't see the day-to-day colour (rumours were that it was Fidelity and foreign brokers who successfully lobbied for this at a time when transaction volumes were very low, an intimations of an increase in turnover following a decrease in transparency).

The position reporting game reveals information that can be beneficial or detrimental depending upon ones objectives and motives. For example, if you are trying to buy 10% of a company at the best prices, reporting after 5% is not in one's interests. On the other hand, if one intends to buy 10%, having bought 5% at lower prices, disclosing the position might attract copy-cat buying that is beneficial from the point of you of having "the market" do some of the subsequent heavy lifting that raises the price, making the initial 5% rather more profitable and validating the purchase decision. However, if one desires to acquire 10% before encouraging the copy-cats to pile in, then reporting requirements clearly creates adverse issues.

When reporting was first enacted in I believe 2003 (and foregive my imprecision as my memory is fraying), Japan was not popular with international investors. In fact, most were underweight from a GDP adn a market cap weighting for all manner of reasons. But for the few who were operating, it revealed valuable information about who was ramping what. It mathced the proverbial name to the face. For when Fidelity was buying a truckload-sized position, a potential short-seller would be wise to recall the words of Jim Croce: "You don't tug on Superman's cape, you don't spit into the wind, you don't pull the mask off that ol' Lone Ranger, and you don;t mess around with Jim!".

Some [foreign] organizations have taken the view that they'll report quarterly, some time after the end of the quarter. And it seems that despite the apprent flaunting of the letter of the regulations, no action has been taken in customary Japanese fashion. Others such as Steel Partners, have complied for obvious reasons that publicizing their now-greater-than-5%-position attracts other buyers hoping for a quick buck. But now, it appears even the "big boys" are fed up with the annoyances of reporting. For beginning last quarter or so, it seemed that rather than institutional investors accumulating positions and reporting them as they accumulated them, brokers were accujmulating them, and anecdotally, shortly thereafter, the broker would report a drop in the position and a "real investor" (Fidelity, Cap Research etc.) would assume ownership. Now, IF I am correct and they are using these methods to obfuscate ownership acumulation until they've achieved their desired quantities, they must in order to do this, be using some option or derivative structure that technically complies with the regulation, but is contrary to the spirit of the regulation. This is of course, the raison d'etre of much of the derivatives market, but nonetheless is disturbing for those that are cannily trying to unmask price manipulations of all variety for fun, public interest, and profit.

The technology exists of course to ascribe meaningful ownership changes - and thereby the potential misuse of material non-public information - with precision and regularity. Bearer shares exist no more, and info is there for public consumption. When will Japanese authorities codify and enforce such regulations with the efficiency we've come to know and admire from this nation? Hmmmm. One would have thought that the Horie affair would have provided sufficient mpetus for change. But shenanigans certainly continue amongst powerful domestic interests, and in such an event, one must wonder for the like of Softbank and others, what unsavoury deeds might be revealed or disrobed in the process.

And, nowhere is this more germane than in the case of reporting large positions to stock exchange regulators around the world generally, and in Japan particularly. Japan seemingly has a love-hatre relationship with transparency. Reading who has bought what and when was a fascinating exercise. On one hand, ownership changes were only detailed twice a year, and even then, only the larger holders either through the YuHo or Toyo Keizaei. So it was long after the fact that one realized who had bought the slugs of stock that vaulted the price an issue by triple digit percent. Yet, at the same time, turnover identification was available on each stock at the end of each day. This was a dead give-away as to whether purchasers were foreign or domestic, sporadic or persistent. The strange mix of obfuscation and transparaency juxtaposed each other.

A few years ago, the authorities decided, for unexplained reasons, not to "fix" this, but to turn it own its head, by eliminating the revelation of who was responsible for what percentage of turnover in a security on a particular day, while instituting a requirement to report ownership positions in a security greater than 5% (and thereafter) within some timely interval that is apparently indecipherable when reviewing the very wide variety in reported actions and compliance. Now, one couldn't see the day-to-day colour (rumours were that it was Fidelity and foreign brokers who successfully lobbied for this at a time when transaction volumes were very low, an intimations of an increase in turnover following a decrease in transparency).

The position reporting game reveals information that can be beneficial or detrimental depending upon ones objectives and motives. For example, if you are trying to buy 10% of a company at the best prices, reporting after 5% is not in one's interests. On the other hand, if one intends to buy 10%, having bought 5% at lower prices, disclosing the position might attract copy-cat buying that is beneficial from the point of you of having "the market" do some of the subsequent heavy lifting that raises the price, making the initial 5% rather more profitable and validating the purchase decision. However, if one desires to acquire 10% before encouraging the copy-cats to pile in, then reporting requirements clearly creates adverse issues.

When reporting was first enacted in I believe 2003 (and foregive my imprecision as my memory is fraying), Japan was not popular with international investors. In fact, most were underweight from a GDP adn a market cap weighting for all manner of reasons. But for the few who were operating, it revealed valuable information about who was ramping what. It mathced the proverbial name to the face. For when Fidelity was buying a truckload-sized position, a potential short-seller would be wise to recall the words of Jim Croce: "You don't tug on Superman's cape, you don't spit into the wind, you don't pull the mask off that ol' Lone Ranger, and you don;t mess around with Jim!".

Some [foreign] organizations have taken the view that they'll report quarterly, some time after the end of the quarter. And it seems that despite the apprent flaunting of the letter of the regulations, no action has been taken in customary Japanese fashion. Others such as Steel Partners, have complied for obvious reasons that publicizing their now-greater-than-5%-position attracts other buyers hoping for a quick buck. But now, it appears even the "big boys" are fed up with the annoyances of reporting. For beginning last quarter or so, it seemed that rather than institutional investors accumulating positions and reporting them as they accumulated them, brokers were accujmulating them, and anecdotally, shortly thereafter, the broker would report a drop in the position and a "real investor" (Fidelity, Cap Research etc.) would assume ownership. Now, IF I am correct and they are using these methods to obfuscate ownership acumulation until they've achieved their desired quantities, they must in order to do this, be using some option or derivative structure that technically complies with the regulation, but is contrary to the spirit of the regulation. This is of course, the raison d'etre of much of the derivatives market, but nonetheless is disturbing for those that are cannily trying to unmask price manipulations of all variety for fun, public interest, and profit.

The technology exists of course to ascribe meaningful ownership changes - and thereby the potential misuse of material non-public information - with precision and regularity. Bearer shares exist no more, and info is there for public consumption. When will Japanese authorities codify and enforce such regulations with the efficiency we've come to know and admire from this nation? Hmmmm. One would have thought that the Horie affair would have provided sufficient mpetus for change. But shenanigans certainly continue amongst powerful domestic interests, and in such an event, one must wonder for the like of Softbank and others, what unsavoury deeds might be revealed or disrobed in the process.

Tuesday, December 19, 2006

Quote of the Day

In an interview with Bloomberg, Ara Hovnanian CEO President of the company bearing his name said:

"We really didn't see it [the housing slowdown] coming...."

He added (scratching his head):

"What's unusual [about the slowdown] this time, is that interest rates are low." "It's unprecendented!"

"Demand has slackened most in areas where prices had gone up the most" (strange, that!! -ed.)

-- Ara Hovnanian, President/CEO Hovnanian Enterprises

My comment: That would be fine if Mr Hovnanian was, say, perhaps a "Boulanger", an Elementary School Arts Teacher, or a Juggler in "Le Cirque du Soleil". But as the President & CEO of one of America's, (and the world's, I might add) largest residential homebuilders, his foresight is rather deficient....

"We really didn't see it [the housing slowdown] coming...."

He added (scratching his head):

"What's unusual [about the slowdown] this time, is that interest rates are low." "It's unprecendented!"

"Demand has slackened most in areas where prices had gone up the most" (strange, that!! -ed.)

-- Ara Hovnanian, President/CEO Hovnanian Enterprises

My comment: That would be fine if Mr Hovnanian was, say, perhaps a "Boulanger", an Elementary School Arts Teacher, or a Juggler in "Le Cirque du Soleil". But as the President & CEO of one of America's, (and the world's, I might add) largest residential homebuilders, his foresight is rather deficient....

Monday, December 18, 2006

Cassandra's Xmas Presents to You

OK, Santa has come early. Of course some will say just "Buy Gold", but the smart investor is always trying to optimize, and do better. After all, bullion yields nothing, is risky, can be confiscated, and has few uses outside the speculative and decorative. Here is a Xmas investment (adn trading) shopping list that should, if nothing else allow the Goldbugs or just the worriers to BOTH invest and sleep better in the evenings.

1. Short High-Grade Copper vs. Long Gold

(Lots more HG1 about than GOLDS. Easier money for those with strong constitutions than phishing bank details from Nebraskans).

2. Long Cheap Japan Domestic Stocks vs Short Expensive US Consumer Discretionary stocks (currency unhedged).

The Easiest money may be gone, but this will continue to pay. Own the sub-book value soon-to-appreciate currency vs. the sector that once again will be ask investor owning it to bend-over (and get the yield pick-up while you wait to offset the high cost of shorting YEN)

3. Long CAD vs. Short GBP

Erosion of USD value vs. contractionary outcome will insure Canada doesn't roll over and so Bank of Canada will not be cutting rates anytime soon. In the race to see who cuts first, BoE will blink first cutting sterling rates before loonies.

4. Long YEN vs. Short Euro

Twenty-percent in 2007 on this one (Take 10% in Q1 if you get it, and put it back on again in July). If it don't happen, random Japanese tourists will be ritually sacrificed on the banks of the Seine.

5. Short USD Bonds

Rebalancing of CB reserves, means some of the distortions in the USD bond market will cease. And since no new taxes until 2008, and no new rate rises in 2007, US fiscal, trade and CA deficits will continue to provide ample reason to short bonds.

6. Short USD Quality Spreads

Short conumer-sensitive junk bonds where a continued retrenchment by consumer from higher energy prices bites and forces cutbacks.

7. Short Nucor vs. Long Newmont

There is an impending surplus of steel. Maybe not as fine as Nuecor's specialty, but nonetheless this trade will pay and pay and pay. Similar rationale to short the physical copper and long the physical bullion. Do it in options (short call vs. long call for the meek and timid).

8. Long Devon (DVN), Anadarko (APC), Apache (APA), Cimarex (CMX), Encana (ECA), Suncor (SU), Conoco-Philips (COP) Chevron (CVX) & Marathon MRO).

All are well south of heavily discounted NPV using low forward oil price estimates. The essential play is one of property rights in that US & Canadian resource property rights - in the absence of world-rogering depression - are most secure. Recent moves in Bolivia, Venezuela, Russia are harbingers of future actions that will see nation-states take greater control. These are wonderful "stores of value" with attractive current yields, trading is discounts, relatively secure. Should be part of any portfolio.

9. Stay Long: Global Sante-Fe (GSF), Diamond Offshore DO), Cleveland-Cliffs (CLF); Raynier (RYN)& PlumCreek (PCL), & Svenska Cell 'B' (SCAB SS), and Sherritt (S CN).

Assets. Assets. Assets. It takes three years to build deepwater rigs like these, and there aren't many out there. Attractive valuations, wonderfully abundant free cashflow, little encumbrances, should continue to make DO & GSF prized assets. Geography will continue to favor CLF over CVRD or BHP for NAm steel. Great balance sheet, and still cheap. RYN & PCL are Timberland LPs that are far south of book, nice current yield, and great assets - the kind the Chinese would love to buy. Bearts thought the Timberland boom passe, but recent transactions (admittedly by RYN) just paid $2200 acre in Texas, goosing implied values substantially.

10. Eastern European (& German) Real Estate.

OK so you feel bad that you didn't buy them when they were giving them away. Shame shame shame. But do not forget that Central Europe was the Center of the Civilized Chistian World for a very long time. Paris and London were hovels in comparison to Prague, Budapest, and Belgrade. Croatia, Serbia, Hungary, Berlin rural Greece, all afford excellent value for those with a long view. When the coming Europe vs. Asia trade wars come, Eastern Europe will continue to prosper as the lower-wage periphery of developed Europe. Europeans will (rightly) prefer to pay a bit more and buy from THEIR periphery where 80% is recycled back into Euro-area economies than from Asia. Farmland, coastal property, and urban locations still will afford attractive long-term appreciations on long-view with acceptable (but rising yields) in the interim.

And with anything left over, just go buy some Titanium, Uranium concentrate, or ultra-pure polysilicon and warehouse it safely.

Peace to all!

1. Short High-Grade Copper vs. Long Gold

(Lots more HG1 about than GOLDS. Easier money for those with strong constitutions than phishing bank details from Nebraskans).

2. Long Cheap Japan Domestic Stocks vs Short Expensive US Consumer Discretionary stocks (currency unhedged).

The Easiest money may be gone, but this will continue to pay. Own the sub-book value soon-to-appreciate currency vs. the sector that once again will be ask investor owning it to bend-over (and get the yield pick-up while you wait to offset the high cost of shorting YEN)

3. Long CAD vs. Short GBP

Erosion of USD value vs. contractionary outcome will insure Canada doesn't roll over and so Bank of Canada will not be cutting rates anytime soon. In the race to see who cuts first, BoE will blink first cutting sterling rates before loonies.

4. Long YEN vs. Short Euro

Twenty-percent in 2007 on this one (Take 10% in Q1 if you get it, and put it back on again in July). If it don't happen, random Japanese tourists will be ritually sacrificed on the banks of the Seine.

5. Short USD Bonds

Rebalancing of CB reserves, means some of the distortions in the USD bond market will cease. And since no new taxes until 2008, and no new rate rises in 2007, US fiscal, trade and CA deficits will continue to provide ample reason to short bonds.

6. Short USD Quality Spreads

Short conumer-sensitive junk bonds where a continued retrenchment by consumer from higher energy prices bites and forces cutbacks.

7. Short Nucor vs. Long Newmont

There is an impending surplus of steel. Maybe not as fine as Nuecor's specialty, but nonetheless this trade will pay and pay and pay. Similar rationale to short the physical copper and long the physical bullion. Do it in options (short call vs. long call for the meek and timid).

8. Long Devon (DVN), Anadarko (APC), Apache (APA), Cimarex (CMX), Encana (ECA), Suncor (SU), Conoco-Philips (COP) Chevron (CVX) & Marathon MRO).

All are well south of heavily discounted NPV using low forward oil price estimates. The essential play is one of property rights in that US & Canadian resource property rights - in the absence of world-rogering depression - are most secure. Recent moves in Bolivia, Venezuela, Russia are harbingers of future actions that will see nation-states take greater control. These are wonderful "stores of value" with attractive current yields, trading is discounts, relatively secure. Should be part of any portfolio.

9. Stay Long: Global Sante-Fe (GSF), Diamond Offshore DO), Cleveland-Cliffs (CLF); Raynier (RYN)& PlumCreek (PCL), & Svenska Cell 'B' (SCAB SS), and Sherritt (S CN).

Assets. Assets. Assets. It takes three years to build deepwater rigs like these, and there aren't many out there. Attractive valuations, wonderfully abundant free cashflow, little encumbrances, should continue to make DO & GSF prized assets. Geography will continue to favor CLF over CVRD or BHP for NAm steel. Great balance sheet, and still cheap. RYN & PCL are Timberland LPs that are far south of book, nice current yield, and great assets - the kind the Chinese would love to buy. Bearts thought the Timberland boom passe, but recent transactions (admittedly by RYN) just paid $2200 acre in Texas, goosing implied values substantially.

10. Eastern European (& German) Real Estate.

OK so you feel bad that you didn't buy them when they were giving them away. Shame shame shame. But do not forget that Central Europe was the Center of the Civilized Chistian World for a very long time. Paris and London were hovels in comparison to Prague, Budapest, and Belgrade. Croatia, Serbia, Hungary, Berlin rural Greece, all afford excellent value for those with a long view. When the coming Europe vs. Asia trade wars come, Eastern Europe will continue to prosper as the lower-wage periphery of developed Europe. Europeans will (rightly) prefer to pay a bit more and buy from THEIR periphery where 80% is recycled back into Euro-area economies than from Asia. Farmland, coastal property, and urban locations still will afford attractive long-term appreciations on long-view with acceptable (but rising yields) in the interim.

And with anything left over, just go buy some Titanium, Uranium concentrate, or ultra-pure polysilicon and warehouse it safely.

Peace to all!

Friday, December 15, 2006

Groundhog Day

Markets have a way wearying even the most enthusiastic and energetic observers. There is a wonderful scene in the Bill Murray film, Groundhog Day where the cynical Murray re-lives the same day over and over as the weatherman who has traveled to the middle of nowehere to present a fluff piece on "Punxatawney Phil", the Pennsylvania rodent whose legendary shadow is renown for predicting whether winter will be short or long. And like Euro/Yen's relentless percolation against all reason and internationalo monetary responsibility, Murray, having delivered the same intro, on the same morning, with the same people, in the same town for the umpteenth time, has lost his will, become, bored, lethargic and even hostile at the absurdity and futility of living the same day over and over and over....

What will break the cycle of this Euro vs. Yen "Groundhog Day"? Asset prices all over continue to roar (excepting perhaps Russian joint-ventures coveted by Russian partners, central government, of friends of Mr Putin), Zimbabwean farmland or Venezuelan Pasture. And Japanese Japanese asset are no exception. Tankan was upbeat, Xmas Bonuses were the highest on record, and shares on the bourse have resumed their ascent. And while the ECB prudently expresses concern (even though most know that it is essentially "hot air"), MoF and BoJ officials continue to stoke concerns about deflation, of Nippon slipping back into recession, with not a public whisper about the Yen carry trade and its role in financing everything from US deficits, renovations to SW3 townhomes, to HF managers' record bids for trophy art.

Martin Wolf presciently foresaw this tenous divergent policy in early 2004 in describing the Fed's necessity to tolerate trade and fiscal deficits with complimentary loose policy as the price for keeping the balls in the air. He accurately predicted the roaring business environment, the growing imbalances, and mercantilist surplusses alongside the temporarily-benign purgatory. However he pointed out that it would, eventually, be threated by ballooning asset prices or growing trade-frictions and protectionism.

We've undoubtedly got the first. Liquidity is so abundant listed US companies are falling prey to LEVERAGED private market buyers at the rate of several per day. Real estate is gallopping again in overbought, overheated and unaffordable markets like UK, Australia and Spain despite tepid retail sales, stagnant employment and real wage growth. A spade must be called a spade, and this phenomenon is a pure monetary phenom. We have now proceeded deep into unprecedented territory, though we are protected from the most vbicious of beasts by Central Banks willingness to hold the dollars. But it is frightening to hear talk of independant Chinese agencies to "manage the assets", or wonder what might become of them should trade frictions rise as they are certainly bound to do.

(Sod's Law: Yen/Euro moves -1% as I finished typing this post)

What will break the cycle of this Euro vs. Yen "Groundhog Day"? Asset prices all over continue to roar (excepting perhaps Russian joint-ventures coveted by Russian partners, central government, of friends of Mr Putin), Zimbabwean farmland or Venezuelan Pasture. And Japanese Japanese asset are no exception. Tankan was upbeat, Xmas Bonuses were the highest on record, and shares on the bourse have resumed their ascent. And while the ECB prudently expresses concern (even though most know that it is essentially "hot air"), MoF and BoJ officials continue to stoke concerns about deflation, of Nippon slipping back into recession, with not a public whisper about the Yen carry trade and its role in financing everything from US deficits, renovations to SW3 townhomes, to HF managers' record bids for trophy art.

Martin Wolf presciently foresaw this tenous divergent policy in early 2004 in describing the Fed's necessity to tolerate trade and fiscal deficits with complimentary loose policy as the price for keeping the balls in the air. He accurately predicted the roaring business environment, the growing imbalances, and mercantilist surplusses alongside the temporarily-benign purgatory. However he pointed out that it would, eventually, be threated by ballooning asset prices or growing trade-frictions and protectionism.

We've undoubtedly got the first. Liquidity is so abundant listed US companies are falling prey to LEVERAGED private market buyers at the rate of several per day. Real estate is gallopping again in overbought, overheated and unaffordable markets like UK, Australia and Spain despite tepid retail sales, stagnant employment and real wage growth. A spade must be called a spade, and this phenomenon is a pure monetary phenom. We have now proceeded deep into unprecedented territory, though we are protected from the most vbicious of beasts by Central Banks willingness to hold the dollars. But it is frightening to hear talk of independant Chinese agencies to "manage the assets", or wonder what might become of them should trade frictions rise as they are certainly bound to do.

(Sod's Law: Yen/Euro moves -1% as I finished typing this post)

Tuesday, December 12, 2006

Sorceror's Apprentice

OK nothing profound today, but I cannot get the image of Disney's fine depiction of Mickey & The Sorceror's Apprentice out of my head as I contemplate the state of Bretton Woods II.

OK nothing profound today, but I cannot get the image of Disney's fine depiction of Mickey & The Sorceror's Apprentice out of my head as I contemplate the state of Bretton Woods II. See our Mickey, charged with cleaning up the world by his Maestro. Being a slacker at heart, he conjures assistance in the form of help from the Asian CBs (depicted here carting away excess dollar reserves), rather than directly tackling the task and undertaking the hard work of adjustment itself. I don't know quite how far one can go with this analogy, but I continue to be amused at the thought of some larger-than-life Volcker-like character re-appearing as "The Sorceror" himself to sternly reproach his apprentice both for his laziness and rather amateurish attempt to rectify the situation with the pathetic application of magic rather than diligence.

Friday, December 08, 2006

Paradoxical Incentives

And so Marshall Wace has raised $2billion from investors for a closed-end vehicle called "MW Tops" that will pursue "hedge fund strategies". I could be accused of professional jealousy - after all, who wouldn't want to win the lottery - but that is precisely what a $2bn closed-end fund is akin to for a manager with an elevated management fee + incentive fee structure.

With no disrespect to Mssrs. Marshall & Wace, who've performed admirably andd consistently over a long period such that their success is unlikely the product of the coin-flipping survivalism. And perhaps they've discovered the "Philosphers' Stone", and imbued it into a fund management method, or engaged sufficiently talented vassals such that performance could survive the principals' extended holidays, sabbaticals to ashrams in India, election campaigns for Parliament, etc. But along with ever-more restrictive gates in top-performing firms such as Citadel, locked in capital seems at odds with the shifting sands inherent to the Fund Management business. The fortunes of even the best firms waxes and wanes with the turnover of personnel, changes in corporate culture and hunger of the founder, principals or key persons, as well as the frequent inability of even the most successful people and firms to change with the times.

All that is fine and understood for someone seeking a firm offering to manage money on flexible terms for modest fees. But the relationship deteriorates assymetrically when one turns over money to a rockstar of finance with little to no recourse, oversight, transparency, covenants against excessive leverage (Citadel is already >10x levered) or risk-taking, or in the case of Citadel, any exit. One cannot simply "vote with their feet" and walk from a heavily gated fund structure. Nor is itan appealing proposition to dump one's closed-end shares into a market where the prevailing price is a hefty 15% to 20% discount to stated NAV, a level of discount frequently seen in the market for less-than-popular closed-end vehicles where one's star manager, investment strategy, or asset-class objective has sunk.

I understand all the arguments for "dedicated capital": preventing investors from doing the "wrong thing", insuring "dry powder" when market chaos (read: opportunity) presents itself, insuring business stability and thus enterprise quality, and so on. Yet there is nothing to protect an investor, from the equally deleterious and known demons of delegated agency investment managent such (for example: hubris, excessive risk-taking, massive errors in judgement, benign fiduciary negligence), save faith itself. And in danger of being a cynic, when I look at "faith" such as UK government's "faith" that competition will insure that public retail energy prices will rise and fal symmetrically, or the faith that companies have thoroughly tested the safety of chemicals inherent in their products, or the veracity of claims that Saddam must be brought down because he possesses weapons of mass destruction, I think one (and investors) would show wisdom in being skeptical that their interests will be equally served and protected, as those interests of the concentrated beneficiaries of such highly-gated or closed end structures. Caveat emptor!

With no disrespect to Mssrs. Marshall & Wace, who've performed admirably andd consistently over a long period such that their success is unlikely the product of the coin-flipping survivalism. And perhaps they've discovered the "Philosphers' Stone", and imbued it into a fund management method, or engaged sufficiently talented vassals such that performance could survive the principals' extended holidays, sabbaticals to ashrams in India, election campaigns for Parliament, etc. But along with ever-more restrictive gates in top-performing firms such as Citadel, locked in capital seems at odds with the shifting sands inherent to the Fund Management business. The fortunes of even the best firms waxes and wanes with the turnover of personnel, changes in corporate culture and hunger of the founder, principals or key persons, as well as the frequent inability of even the most successful people and firms to change with the times.

All that is fine and understood for someone seeking a firm offering to manage money on flexible terms for modest fees. But the relationship deteriorates assymetrically when one turns over money to a rockstar of finance with little to no recourse, oversight, transparency, covenants against excessive leverage (Citadel is already >10x levered) or risk-taking, or in the case of Citadel, any exit. One cannot simply "vote with their feet" and walk from a heavily gated fund structure. Nor is itan appealing proposition to dump one's closed-end shares into a market where the prevailing price is a hefty 15% to 20% discount to stated NAV, a level of discount frequently seen in the market for less-than-popular closed-end vehicles where one's star manager, investment strategy, or asset-class objective has sunk.

I understand all the arguments for "dedicated capital": preventing investors from doing the "wrong thing", insuring "dry powder" when market chaos (read: opportunity) presents itself, insuring business stability and thus enterprise quality, and so on. Yet there is nothing to protect an investor, from the equally deleterious and known demons of delegated agency investment managent such (for example: hubris, excessive risk-taking, massive errors in judgement, benign fiduciary negligence), save faith itself. And in danger of being a cynic, when I look at "faith" such as UK government's "faith" that competition will insure that public retail energy prices will rise and fal symmetrically, or the faith that companies have thoroughly tested the safety of chemicals inherent in their products, or the veracity of claims that Saddam must be brought down because he possesses weapons of mass destruction, I think one (and investors) would show wisdom in being skeptical that their interests will be equally served and protected, as those interests of the concentrated beneficiaries of such highly-gated or closed end structures. Caveat emptor!

Monday, December 04, 2006

Mr Yen says: "Not Yet"

Despite the rollicking Euro vs. Yen movement, Dr Eisuke Sakakibara was quoted today by Bloomberg as saying that the chance of a year-end BoJ rate hike remains less than 50% (30% to 40% was his more precise prognostication). And, if so, it would hardly count a turning of the proverbial screw at a mere 0.25%. Modulating the use of Yen for all manner of ex-Japan, ex-Yen finance seems not to be an objective of the MoF, the BoJ, or, for that matter, anyone else in the world who matters.

It's ironic that everyone sees the Yen lower v. the dollar in 2007, lost of people are bearish on the dollar now, yet almost no one seems willing to say "Yes, it's now Go Long Yen!!". It this because everyone has become a is a momentum or feedback trader? Are there no more contrarians left in the world? Whatever the case, it is a situation that suits TeamJapan just fine.

It's ironic that everyone sees the Yen lower v. the dollar in 2007, lost of people are bearish on the dollar now, yet almost no one seems willing to say "Yes, it's now Go Long Yen!!". It this because everyone has become a is a momentum or feedback trader? Are there no more contrarians left in the world? Whatever the case, it is a situation that suits TeamJapan just fine.

Friday, December 01, 2006

Kwai Bridge & The Yen

This is NOT a Japanese hate blog. I truly like and admire the Japanese people and culture. Much of it anyway. And for years I have given super-human credit to the MITI & MoF (Ministry of Finance) for prescience, planning and organization. Yet I am having my doubts.

Yesterday I watched a PBS special on the horror and brutality employed by the Japanese in building of a Southeast Asian railway, most famously known for "The Bridge Over the River Kwai". And while historically, the allies may remember it for the unlawful use of prisoners in the construction process, nearly 100,000 Asians (mostly indiginous Malays) perished i their efforts as well. Of course this may not be a surprise given Manchuria was no secret. Nor was their pathetic behaviour in Korea, and, for that matter, anywhere else in Asia they happened to land and occupy undocumented. 60 years hence, Asians remain sensitive, and unforgetful about war-time atrocities, and for good reason: Japanese behaviour was atrocious!

Yet, many Japanese (both nationalists and otherwise) do not seem to "get" foreign sensitivity regarding visits to Yasakuni, lame textbook accounts about more or less objective history, or their seeming unwillingness to be culpabable to historical events, in the same way they eagerly seize culpablility to other Japanese, on behalf of things Japanese. This is puzzling to me, and really struck home when watching the interviews with the now-elderly Japanese engineers and soldiers who took part and oversaw the railways construction, and it's brutal consequences. They seemed to abnegate all responsibility. Yes, they admitted it was war, and things were done in the name of war. But to a man, they denied prisoners were forced into labour. They suggested prisoners' deaths were the result of "bad rice" or other such nonsense. Were these denials "real"? Sure they were concern4ed about war-crimes, and preesent-day "shame" of being brandished so. But did they actually believe this? Was it a defense mechanism of the human psyche constructed to excise and quarantine the unthinkable and the unimaginably horrible?

All which makes me think about the credit I have been attributing to the MITI & MOF and whether it is mis-placed. Just how cynical "is" the weak-yen policy? How much do policy-makers really believe that ZIRP is somehow benefitting local economic conditions, Capex, or credit take-up by the average Japanese household (who in any event are large net savers)?? Perhaps, they really believe it themselves! And, if so, what will it take to change their behaviour from parochially tribal (and damaging to the international monetary system), to one more global and responsible in nature?? If the financial system blows up, could Omi, Ota, Fukui, or Tanigaki (not to mention George Bush), be termed an "economic war criminals"?

Yesterday I watched a PBS special on the horror and brutality employed by the Japanese in building of a Southeast Asian railway, most famously known for "The Bridge Over the River Kwai". And while historically, the allies may remember it for the unlawful use of prisoners in the construction process, nearly 100,000 Asians (mostly indiginous Malays) perished i their efforts as well. Of course this may not be a surprise given Manchuria was no secret. Nor was their pathetic behaviour in Korea, and, for that matter, anywhere else in Asia they happened to land and occupy undocumented. 60 years hence, Asians remain sensitive, and unforgetful about war-time atrocities, and for good reason: Japanese behaviour was atrocious!

Yet, many Japanese (both nationalists and otherwise) do not seem to "get" foreign sensitivity regarding visits to Yasakuni, lame textbook accounts about more or less objective history, or their seeming unwillingness to be culpabable to historical events, in the same way they eagerly seize culpablility to other Japanese, on behalf of things Japanese. This is puzzling to me, and really struck home when watching the interviews with the now-elderly Japanese engineers and soldiers who took part and oversaw the railways construction, and it's brutal consequences. They seemed to abnegate all responsibility. Yes, they admitted it was war, and things were done in the name of war. But to a man, they denied prisoners were forced into labour. They suggested prisoners' deaths were the result of "bad rice" or other such nonsense. Were these denials "real"? Sure they were concern4ed about war-crimes, and preesent-day "shame" of being brandished so. But did they actually believe this? Was it a defense mechanism of the human psyche constructed to excise and quarantine the unthinkable and the unimaginably horrible?

All which makes me think about the credit I have been attributing to the MITI & MOF and whether it is mis-placed. Just how cynical "is" the weak-yen policy? How much do policy-makers really believe that ZIRP is somehow benefitting local economic conditions, Capex, or credit take-up by the average Japanese household (who in any event are large net savers)?? Perhaps, they really believe it themselves! And, if so, what will it take to change their behaviour from parochially tribal (and damaging to the international monetary system), to one more global and responsible in nature?? If the financial system blows up, could Omi, Ota, Fukui, or Tanigaki (not to mention George Bush), be termed an "economic war criminals"?

Thursday, November 30, 2006

Euro-Yen at the Eleventh & a Half Hour

What are nation-states to do when markets imperfectly reflect the state of the world consistent with longer-term equilibrium? Witness the Japanese Yen vs. The Euro in the accompanying graph. What are we to make of it?

The market, according to pundits far and wide, ostensibly is focused on "interest rate differentials", and the forecasted rate of change thereof in the immediate period. Employing this line of reasoning, it would seem that the market is "acting rationally" eschewing Yen in favour of Euro's. In earlier days this might be wholly understandable since cycles might be distinctly out of phase. But globalization has changed this, increasing economic correlation and business cycle synchronization. Sure fiscal policies differ, and demographics might be divergent. But the logical question to ask is: Why might the European Central Bankers believe that 4% rate of interest is imminently appropriate, whilst the BoJapan's boffins (& MoFo's) believe 1% is too high?

Japanese asset prices are rising smartly - both property (commercial & residential)and shares. Corporate profits are surging. Capital investment increasing. Orders robust. Exports surging. Unemployment low. Government deficits large (>5%GDP). All the above are sure signs that things are pretty damn alright, irrespective of 0.5% core CPI still apparently deemed too low. Europe on the other hand, has less than 3% GDP fiscal deficits, much higher, but decreasing unemployment, surging asset markets, especially commercial and residential property (making some believe there is a bubble), growing private-sector debt, growing capex, roughly balanced trade accounts, and inflation that when incorporating asset prices, is growing and too high for policy makers to countenance.

So why with all this slack in employment, is inflation rearing up in Europe, but not Japan? Why are the Europeans more concerned about inflation or the Japanese with >5% fiscal gaps and near-ZIRP, not more puzzled by why with loose fiscal and loose monetary policy and rollicking asset markets, they are not generating more inflation at home? And if THAT combination of events is not generating goods-price inflation at home, would tighter monetary and fiscal policy really have a negative impact? And, if so, would this be bad for a nation that is is generating incredible dollops of income on overseas assets and FDI?

I think that what markets are not expressing, (rightfully since pissing in the wind is unpleasant in the best of times)) is that betting against the central bank and authorities of the world's second largest economy is a "mugs game". For the the world's central banks - at the moment - are working at different purposes. The US FRB is spinelessly schizo from dual irreconciliable mandates, erring on the side of soft money. The ECB is independently pursuing its mandate, it too erring on the side of soft money, though helped enormously by the saner fiscal policies, forward-thinking energy policy & taxes, and thankfully more balanced trade account, and manufacturing sectors. The BoJ, however, sits alone at the opposite pole to the ECB: politically compromised to TeamJapan, cynically selfish global citizen insofar as they maintain a ZIRP policy that matters not in the least to Japanese demand for credit, but which insures the YEN will be the global funding currency of choice to offset their surplusses and insure that TeamJapan losses not an iota of competitiveness to their Asian peers and would-be competitors. THAT is why the yen has deteriorated over the course of the past four years. THAT is why I loathe the BoJ's inaction, and the MoF's continued demaoguery regarding the impact of higher rates, for the only real impact of higher rates would be prevent the YEN from being the financing currency of choice for global carry, resulting in a higher Yen, resulting in lower corporate profits and potentially deflation of the benign adn unpernicious kind that results from productivity gains, plateuing demographics, and a geographical location adjacent to the largest deflationary force the world has ever seen.

China bears some blame here. For China, rather than be accumulating dollars, should be selling dollars and buying Yen, driving the Yen/Euro and Yen /dollar towards equilibruim amongst the crosses, and preparing for what the eventual acscent of the RMB (and the GCC currencies) relative to the entire OECD currency panpoly.

The market, according to pundits far and wide, ostensibly is focused on "interest rate differentials", and the forecasted rate of change thereof in the immediate period. Employing this line of reasoning, it would seem that the market is "acting rationally" eschewing Yen in favour of Euro's. In earlier days this might be wholly understandable since cycles might be distinctly out of phase. But globalization has changed this, increasing economic correlation and business cycle synchronization. Sure fiscal policies differ, and demographics might be divergent. But the logical question to ask is: Why might the European Central Bankers believe that 4% rate of interest is imminently appropriate, whilst the BoJapan's boffins (& MoFo's) believe 1% is too high?

Japanese asset prices are rising smartly - both property (commercial & residential)and shares. Corporate profits are surging. Capital investment increasing. Orders robust. Exports surging. Unemployment low. Government deficits large (>5%GDP). All the above are sure signs that things are pretty damn alright, irrespective of 0.5% core CPI still apparently deemed too low. Europe on the other hand, has less than 3% GDP fiscal deficits, much higher, but decreasing unemployment, surging asset markets, especially commercial and residential property (making some believe there is a bubble), growing private-sector debt, growing capex, roughly balanced trade accounts, and inflation that when incorporating asset prices, is growing and too high for policy makers to countenance.

So why with all this slack in employment, is inflation rearing up in Europe, but not Japan? Why are the Europeans more concerned about inflation or the Japanese with >5% fiscal gaps and near-ZIRP, not more puzzled by why with loose fiscal and loose monetary policy and rollicking asset markets, they are not generating more inflation at home? And if THAT combination of events is not generating goods-price inflation at home, would tighter monetary and fiscal policy really have a negative impact? And, if so, would this be bad for a nation that is is generating incredible dollops of income on overseas assets and FDI?

I think that what markets are not expressing, (rightfully since pissing in the wind is unpleasant in the best of times)) is that betting against the central bank and authorities of the world's second largest economy is a "mugs game". For the the world's central banks - at the moment - are working at different purposes. The US FRB is spinelessly schizo from dual irreconciliable mandates, erring on the side of soft money. The ECB is independently pursuing its mandate, it too erring on the side of soft money, though helped enormously by the saner fiscal policies, forward-thinking energy policy & taxes, and thankfully more balanced trade account, and manufacturing sectors. The BoJ, however, sits alone at the opposite pole to the ECB: politically compromised to TeamJapan, cynically selfish global citizen insofar as they maintain a ZIRP policy that matters not in the least to Japanese demand for credit, but which insures the YEN will be the global funding currency of choice to offset their surplusses and insure that TeamJapan losses not an iota of competitiveness to their Asian peers and would-be competitors. THAT is why the yen has deteriorated over the course of the past four years. THAT is why I loathe the BoJ's inaction, and the MoF's continued demaoguery regarding the impact of higher rates, for the only real impact of higher rates would be prevent the YEN from being the financing currency of choice for global carry, resulting in a higher Yen, resulting in lower corporate profits and potentially deflation of the benign adn unpernicious kind that results from productivity gains, plateuing demographics, and a geographical location adjacent to the largest deflationary force the world has ever seen.

China bears some blame here. For China, rather than be accumulating dollars, should be selling dollars and buying Yen, driving the Yen/Euro and Yen /dollar towards equilibruim amongst the crosses, and preparing for what the eventual acscent of the RMB (and the GCC currencies) relative to the entire OECD currency panpoly.

Wednesday, November 29, 2006

Bully Steals Candy From Baby

So American carpetbagger, Steel Partners, has managed to extract tribute from another Japanese management, in the form of Nissin Foods (TSE Code#2897) offer to purchase Myojo's (TSE Code#2900) shares from any and all comers at a heft premium to an already ramped-up market share price. Steel will undoubtedly tender. Nissin trumpeted the transaction benefits of a rather nebulous-sounding tie-up (surely meaning creation of a noodle cartel or price fixing oligopoly). But in their statement, they also unashamedly described their actions as protecting the many and varied Myojo constituents such as suppliers, customers, employees and management.

Not content to "cut & run" with the profits, nor satisfied with the greenmail gains, Steel reported today a 6% stake in Nissin itself, apparently as a result of the sub-optimal move of buying shares at a premium, but not taking the company over.

Greenmail IS effective in Japan. However, the Japanese will not continue to be extorted forever. What they (they being Japan Inc.) should do is let Steel actually succeed in one or so of their tenders since Steel has no strategic business rationale as cash acquirer, not to mention a probable shortfall in capital to actually finance the tender(s). It is a classic case of "be careful what you wish for". Let them, in the process of shaking down management, actually gorge themselves on a couple of chunky (but hard to digest) morsels (already ramped with expensive valuations) and see how they enjoy rolling up their sleeves as sole owner, or whether or not they have a trade buyer lined-up in the event of success. For the best way to deal with a bully is to call him out and embarass him (or her) in front of their peers for all to see their hollowness.

Could Japan stomach a few corporate sacrifices? Perhaps they should countenance such an offering to Steel, and then let labor and government ministries go wild and harass them thereafter as a not-so-subtle message to copycats to think carefully. For if they let Steel achieve even a modicum of success shaking down the system, there will be no shortage of imitators shaking up the share registers of listed companies something that would certainly NOT be in the interests of management, nor many other constituents, or even longer-term affiliated investors where shorter-term profit maximization is not at the top of the list of ownership objectives.

Not content to "cut & run" with the profits, nor satisfied with the greenmail gains, Steel reported today a 6% stake in Nissin itself, apparently as a result of the sub-optimal move of buying shares at a premium, but not taking the company over.

Greenmail IS effective in Japan. However, the Japanese will not continue to be extorted forever. What they (they being Japan Inc.) should do is let Steel actually succeed in one or so of their tenders since Steel has no strategic business rationale as cash acquirer, not to mention a probable shortfall in capital to actually finance the tender(s). It is a classic case of "be careful what you wish for". Let them, in the process of shaking down management, actually gorge themselves on a couple of chunky (but hard to digest) morsels (already ramped with expensive valuations) and see how they enjoy rolling up their sleeves as sole owner, or whether or not they have a trade buyer lined-up in the event of success. For the best way to deal with a bully is to call him out and embarass him (or her) in front of their peers for all to see their hollowness.

Could Japan stomach a few corporate sacrifices? Perhaps they should countenance such an offering to Steel, and then let labor and government ministries go wild and harass them thereafter as a not-so-subtle message to copycats to think carefully. For if they let Steel achieve even a modicum of success shaking down the system, there will be no shortage of imitators shaking up the share registers of listed companies something that would certainly NOT be in the interests of management, nor many other constituents, or even longer-term affiliated investors where shorter-term profit maximization is not at the top of the list of ownership objectives.

Wednesday, November 22, 2006

Is There Really a Goldilocks?

Some things to ruminate upon:

1. What's the outcome of a tug-o'-war between a falling dollar and Roubini-esque property-led slackening of US domestic demand, and the interaction of the two, upon the dollar price of oil.

2. Ponder whether US rates can survive in their current purgatory-like trading range once the markets smell dollar blood?

3. What is the probability of a genuine Goldilocks scenario including lower energy prices, muted inflation, natural correction in US & global imbalances without contractionary policy and outcome?

4. Could it be that Historical Cap Rates in US Commercial Real Estate and residential housing were, historically speaking, too low, and we are witnessing not a "bubble" nor "flight to hard assets" but simply a re-rating or semi-permanent state-change to higher (albeit sustainably so) valuations ??

5. Will anyone muster the courage to "call out" the BoJ & MoF for their not-so-benign-neglect in letting the Yen slide by >35% vs. the Euro since 2002?

1. What's the outcome of a tug-o'-war between a falling dollar and Roubini-esque property-led slackening of US domestic demand, and the interaction of the two, upon the dollar price of oil.

2. Ponder whether US rates can survive in their current purgatory-like trading range once the markets smell dollar blood?

3. What is the probability of a genuine Goldilocks scenario including lower energy prices, muted inflation, natural correction in US & global imbalances without contractionary policy and outcome?

4. Could it be that Historical Cap Rates in US Commercial Real Estate and residential housing were, historically speaking, too low, and we are witnessing not a "bubble" nor "flight to hard assets" but simply a re-rating or semi-permanent state-change to higher (albeit sustainably so) valuations ??

5. Will anyone muster the courage to "call out" the BoJ & MoF for their not-so-benign-neglect in letting the Yen slide by >35% vs. the Euro since 2002?

Hey Joe! Me so pretty.

What I have to say won't take long:

Japanese stocks, excluding the whimisically thematic, the detritus, and the overly-glamorous, are remarkably cheap in comparison other assets. Factor in the embedded in-the-money currency appreciation option (for non-Yen-based investors since the BoJ will eventually relent), the oligopolistic, or in many cases, near-monpolistic nature of many of their edxport specializations, the low multiples to the hard (and increasingly scarce) underlying assets, as well as in relation to forecast earnings potential, free cash flow generated as well as relative to enterprise value, not to mention relative to replacement value, tossing in the meaingfully large dollops of accounting conservatism (i.e. significant R&D & Advertising that depresses current earnings in favour of future earnings), the benefits of industrial policies and corporate relief that result from national socialization of pensions & healthcare, and one has a compelling case for the shares of such enterprises hedging much monetary devaluation, whilst offering diminished risk should things not really pan out as currently expected.

Skeptics (and those who are, if not short, not long) will chime that there is no "catalyst", but this is untrue. The catalyst is rising asset prices, global relative valuation, continued global economic growth, and no pullback in China until after the 2008 Olympics. Yes, there remains issues for the really meek: transparency & accounting integrity, liquidty, stock supply overhangs in the hands of government, reduced shareholder rights and the cultural heeding of multiple constituencies that have profit-diminishing attributes during slack times, and the effect of dollar devaluation upon competitiveness.

All that and current index-price softness notwithstanding, relative to many other assets, they remain attractive, and if nothing else, will soon (and again) attract buyers - portfolio investors, pension funds, domestics, and petro-dollar earners - that will provide, at the very least, a quick turn with attractive risk v. reward to the bold, though probably larger and more sustained gains over the ensuing 12 months.

Japanese stocks, excluding the whimisically thematic, the detritus, and the overly-glamorous, are remarkably cheap in comparison other assets. Factor in the embedded in-the-money currency appreciation option (for non-Yen-based investors since the BoJ will eventually relent), the oligopolistic, or in many cases, near-monpolistic nature of many of their edxport specializations, the low multiples to the hard (and increasingly scarce) underlying assets, as well as in relation to forecast earnings potential, free cash flow generated as well as relative to enterprise value, not to mention relative to replacement value, tossing in the meaingfully large dollops of accounting conservatism (i.e. significant R&D & Advertising that depresses current earnings in favour of future earnings), the benefits of industrial policies and corporate relief that result from national socialization of pensions & healthcare, and one has a compelling case for the shares of such enterprises hedging much monetary devaluation, whilst offering diminished risk should things not really pan out as currently expected.

Skeptics (and those who are, if not short, not long) will chime that there is no "catalyst", but this is untrue. The catalyst is rising asset prices, global relative valuation, continued global economic growth, and no pullback in China until after the 2008 Olympics. Yes, there remains issues for the really meek: transparency & accounting integrity, liquidty, stock supply overhangs in the hands of government, reduced shareholder rights and the cultural heeding of multiple constituencies that have profit-diminishing attributes during slack times, and the effect of dollar devaluation upon competitiveness.

All that and current index-price softness notwithstanding, relative to many other assets, they remain attractive, and if nothing else, will soon (and again) attract buyers - portfolio investors, pension funds, domestics, and petro-dollar earners - that will provide, at the very least, a quick turn with attractive risk v. reward to the bold, though probably larger and more sustained gains over the ensuing 12 months.

Monday, November 20, 2006

Optimism or Cynicism ?!?!

Question:

Is the fascination for commercial real estate, infrastructure and other hard assets a cold and calculating appraisal of the prevailing political economy that yields a high-probability scneario for more of the same: low interest rates, continued fiscal expansion, yet more current account, trade deficits & industrial hollowing giving way to further asset-price inflation WITHOUT limited imported-goods-price inflation or an interest-rate or currency accident??

Or is the continued run-up in asset prices simply the so-called savings glut and its attendant late-cycle cascades, in combination with what are currently low real interest rates combined with FX & interest-rate stasis, that is causing the herd (even the smart herd) to perhaps myopically "use it or lose it"??

My own money is [wrongly, to date I must admit] on the latter. Though other historically prescient investors have shyed away from the party (LA's Colony Capital Leucadia's Steinberg, Baupost's Klarman, etc.), today, the ranks are joined by Sam Zell (Equity Office Props), and more recently, David Geffen (who dumped a significant chunk of his art collection). While betting against either Blackstone or Carlyle hasn't, in aggregate, been extraordinarily rewarding, with the frenzy and prices-paid along with assumed leverage accelerating, one would be forgiven for wondering whether this stampede into large-scale leveraged asset acquisition is a bold statement of unbridled optimism or an ultimate statement "to be short paper & long assets" because the end of the BWII regime is nigh. Comments please!

Is the fascination for commercial real estate, infrastructure and other hard assets a cold and calculating appraisal of the prevailing political economy that yields a high-probability scneario for more of the same: low interest rates, continued fiscal expansion, yet more current account, trade deficits & industrial hollowing giving way to further asset-price inflation WITHOUT limited imported-goods-price inflation or an interest-rate or currency accident??

Or is the continued run-up in asset prices simply the so-called savings glut and its attendant late-cycle cascades, in combination with what are currently low real interest rates combined with FX & interest-rate stasis, that is causing the herd (even the smart herd) to perhaps myopically "use it or lose it"??

My own money is [wrongly, to date I must admit] on the latter. Though other historically prescient investors have shyed away from the party (LA's Colony Capital Leucadia's Steinberg, Baupost's Klarman, etc.), today, the ranks are joined by Sam Zell (Equity Office Props), and more recently, David Geffen (who dumped a significant chunk of his art collection). While betting against either Blackstone or Carlyle hasn't, in aggregate, been extraordinarily rewarding, with the frenzy and prices-paid along with assumed leverage accelerating, one would be forgiven for wondering whether this stampede into large-scale leveraged asset acquisition is a bold statement of unbridled optimism or an ultimate statement "to be short paper & long assets" because the end of the BWII regime is nigh. Comments please!

Saturday, November 11, 2006

Saturday's Thoughts

"The optimist proclaims we live in the best of all possible worlds; and the pessimist fears this is true."

- James Branch Cabell in 'The Siilver Stallion', 1926

"The liberals can understand everything but people who don't understand them."

- Lenny Bruce

"Conservative, (n.): a statesman who is enamoured of existing evils, as distinguished from the Liberal who wishes to replace them with others.

- Ambrose Bierce

"Credit...is the only ennduring testament to man's confidence in man."

- James Blish

"The cure for admiring the House of Lords" is to go look at it"

- Walter Bagehot

"It is easier to fight for one's principles than live up to them"

- Alfred Adler (1939)

"Democracy is the art of saying "Nice Doggie" until you find a rock"

- Will Roger

- James Branch Cabell in 'The Siilver Stallion', 1926

"The liberals can understand everything but people who don't understand them."

- Lenny Bruce

"Conservative, (n.): a statesman who is enamoured of existing evils, as distinguished from the Liberal who wishes to replace them with others.

- Ambrose Bierce

"Credit...is the only ennduring testament to man's confidence in man."

- James Blish

"The cure for admiring the House of Lords" is to go look at it"

- Walter Bagehot

"It is easier to fight for one's principles than live up to them"

- Alfred Adler (1939)

"Democracy is the art of saying "Nice Doggie" until you find a rock"

- Will Roger

Wednesday, November 08, 2006

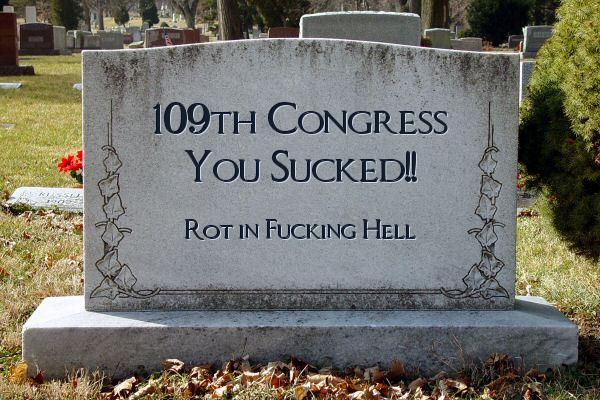

Republican Congress Poetry Corner

(with apologies to EJ Thribb aged 11-1/2)

So Farewell

Then 109th

Congress

Your Mandate

has been

Iraqified,

Abramoffed,

and Foleyed.

Gay Marriage

and Right-

To-Life Bans

Thankfully Unrequited

like Unexploded

Cluster Bombs.

"Everyday Low

Prices"

was your

Catchphrase.

Parochial Greed

and

Total Utter Disregard

For The Public Interest

is Your Legacy

What will you do

now?

Cleaning latrines

is far

too skilled.

'Tis a Shame

My Taxes

Will Pay

Your

Pension.

Tuesday, November 07, 2006

Sadistic Narcissistic Rally

The Bloomberg News headline reads: "US STOCKS ADVANCE ON PROSPECTS OF POST-ELECTION GRIDLOCK", which strikes me as rather, well, disgusting. For, so the logic goes, with gridlock comes more of the the same. Essentially, more large budget deficits, no new taxes, no new energy taxes, no energy policy, no universal healthcare, more military spending, no pharmaceutical regulation, no attempt to rectify international imbalances, and certainly no policy initiatives to attempt to deal with any of the structural risks to international monetary system. It does mean, more inflation, continued negative real interest rates, all of which [for the immediate moment] is the perfect environment for stocks, not to mention all other assets, hard or soft. Under the Gridlock scenario, optimists can look forward to the housing slump being rather shallow for house prices in nominal terms will not fall very much, even if turnover drops. And as inflation accelerates (though interest rates lag with the Fed squarely behind the curve), housing inventories will be consumed as they begin to look attractive once again.

All which conjures images of sleazy "Cock fights", the Gladiators in the Forum of Rome, "bare-knuckle-boxing" or Smash-up Derby" where inexplicable sadism is rife and the seeming focal point of spectators' (or in our case Stock Traders & Investors') maccabre pleasure. Keep an eye out for Emperor Nero, for his is surely lurking nearby.

All which conjures images of sleazy "Cock fights", the Gladiators in the Forum of Rome, "bare-knuckle-boxing" or Smash-up Derby" where inexplicable sadism is rife and the seeming focal point of spectators' (or in our case Stock Traders & Investors') maccabre pleasure. Keep an eye out for Emperor Nero, for his is surely lurking nearby.

The Forest and "Cheap" Trees

I will tell you a personal secret: I become rather anxious when asset prices rise far and fast. This is partly because I hold the opinion that coordinated asset price rises are somewhat self-extinguishing in an environment of already leveraged households, already appreciated assets and rather largely indebted governments. But it is also because I hold some non-hard asset financial assets (because of what I believe to be the elevated probability of the above), and so become relatively poorer with each additional upwards vault. And as behavioural finance researchers have shown, it is indeed one's relative performance that produces anxiety.

And as I look around today, I see all asset prices doing moonshots: Global shares of virtually all sectors; Credit spreads at cyclically narrow levels; real estate of all manner in most countries at post-war peaks in terms of affordability multiples, while cap rates for commercial real estate the world over are near all-time lows. So dire is the cap rate conundrum, and perhaps so certain that the rates won't go up and that the only way to earn an incremental nickel is to lever up that Morgan Stanley recently launched the largest aggressively-leveraged real estate Fund ever seen by mankind. Art from van Gogh, Klimt to Jackson Pollock is valued in the triple-digits of millions, while even some mickingly absurdly modernist art is changing hands in the millions. Undeveloped land is raging. Media content such as recording and film libraries too are garnering impressive valuations, as is agricultural land and orchards. Infrastructure is booming (also with copious amounts of leverage). Antiques, too, are on a rampage, as anyone who's watched Antiques Roadshow can attest. Stamps, coins, curio collections of dubious pedigree, vintage cars, sports memorobilia all gallopping. Commodities of all sorts from precious & metals to softs and foodstuff are up up up.

But my realm is Japan, in general, and Japanese public equities in particular. And here, too, I will share another secret with you: despite raging asset prices the world over in every asset class, in virtually every region (except perhaps North Korea, Zimbabwe & Moldova), slightly more than 30% of listed Japanese public companies are trading south of stated "Book Value" as reported at the end of the latest fiscal year. This is approximately 1225 enterprises out of perhaps approximately 3800, not including those with negative book values. By way of comparison, the US market is, as of last night, sporting nearly 250 listed companies out of nearly 6,800 (using a $50mm market cap cut-off to avoid Chap-11 reorgs). This is a miniscule 3.7% of US listed companies trading sub-book.

Now there remains some caveats: some of these companies are really shitty, detroying shareholder value as prodigious rates. Others are merely illiquid - so illiquid that it might an entire year to acquire but a few percent of the shares outstanding. Another calss are small...in some cases really small...so small that many a hedge fund manager could buy them with their credit card! (ok this is an exaggeration). Yet others have small floats and /or concentrated ownership that they are little more than listed holding companies, and being a shareholder in a Japanese enterprise is trying enough, even before having to countenance being a minority shareholder in a Japanese Company.

To be fair, American companies all suffer from many of the same shortfalls. And perhaps, because the "best and brightest" and the "smartest guys in the room" are engaged in finance rather than engineering, the market is more picked-over, so the probability that a company that is trading sub-book is, in fact, defective is much higher than in Japan, where it is likely to be suffering from inattention, insufficient affection, and general benign neglect.

Nevertheless, 1225 (33%!!) is a large number, so this patch of forest must contain, if nothing else, a lot of assets. And since assets are such the rage these days, the question arises as to how long such potential bargains will remain, especially with money supplies the world over run amok, real rates near zero or negative on any kind of realistic inflation measure NOT calculated by the US BLS?

So perhaps next week, I will introduce a new investment fund called "Assets-'r-Us", and we will blindly buy the entire 100-acre wood, dregs and all, under the mantra: "I don't know, and I don't care, but if it's an asset, lift the offer....". Of course, these assets perhaps should be cheap, and the anomaly could very well be that all other assets are poised to collapse under the weight of their own prices and, the tighter monetary polciy that is imminent, and the contractionary effect of the inevitably deterministic rise in US energy adn income taxes.